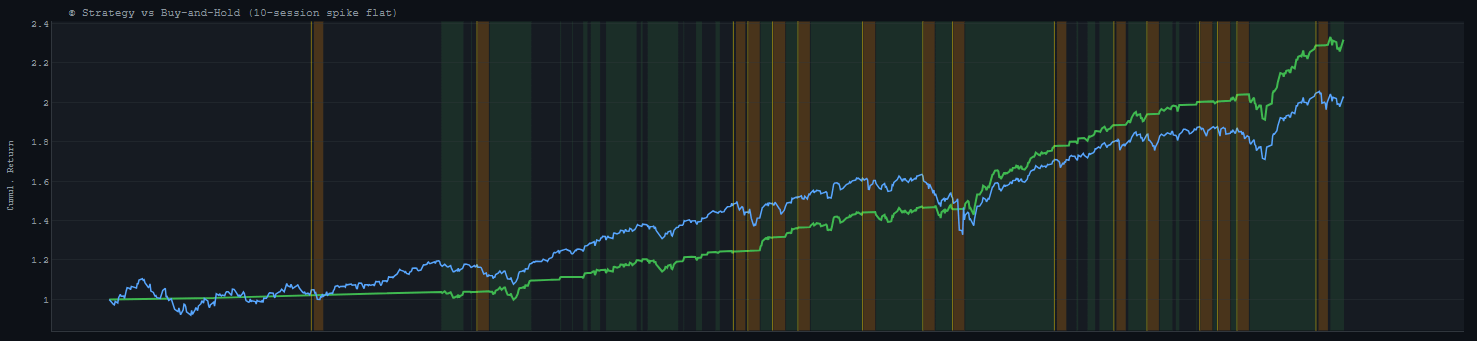

A Quiet Rally Nobody Was Watching

The market had its strongest breadth week of the summer — on a holiday half-week when everyone had already left for the beach. And the sector leading it wasn't the one you'd guess.

Here’s a thing about markets that took me years to recognize and trust the simplicity of: the most important weeks are often the quiet rangebound ones. Before building the definitive platform for uncovering institutional participation, I saw “indecision” in the days and weeks when price washed over a range, unable to breakout. What I now see is deliberate development of price zones where the largest players are positioning for the next move. These moments frustrate retail who want endless trends in both directions but are crucial for engineering the liquidity needed by institutions to paint the next leg. Yes, the days with the screaming headlines and the record volume are part of that liquidity engine, but don’t sleep on the quiet ones, when the desks are half-staffed and nobody’s paying attention, and the money does what it actually wants to do instead of what it wants to be seen doing.

This was one of those weeks. It’s story time…

Start with the number, because the number is the story

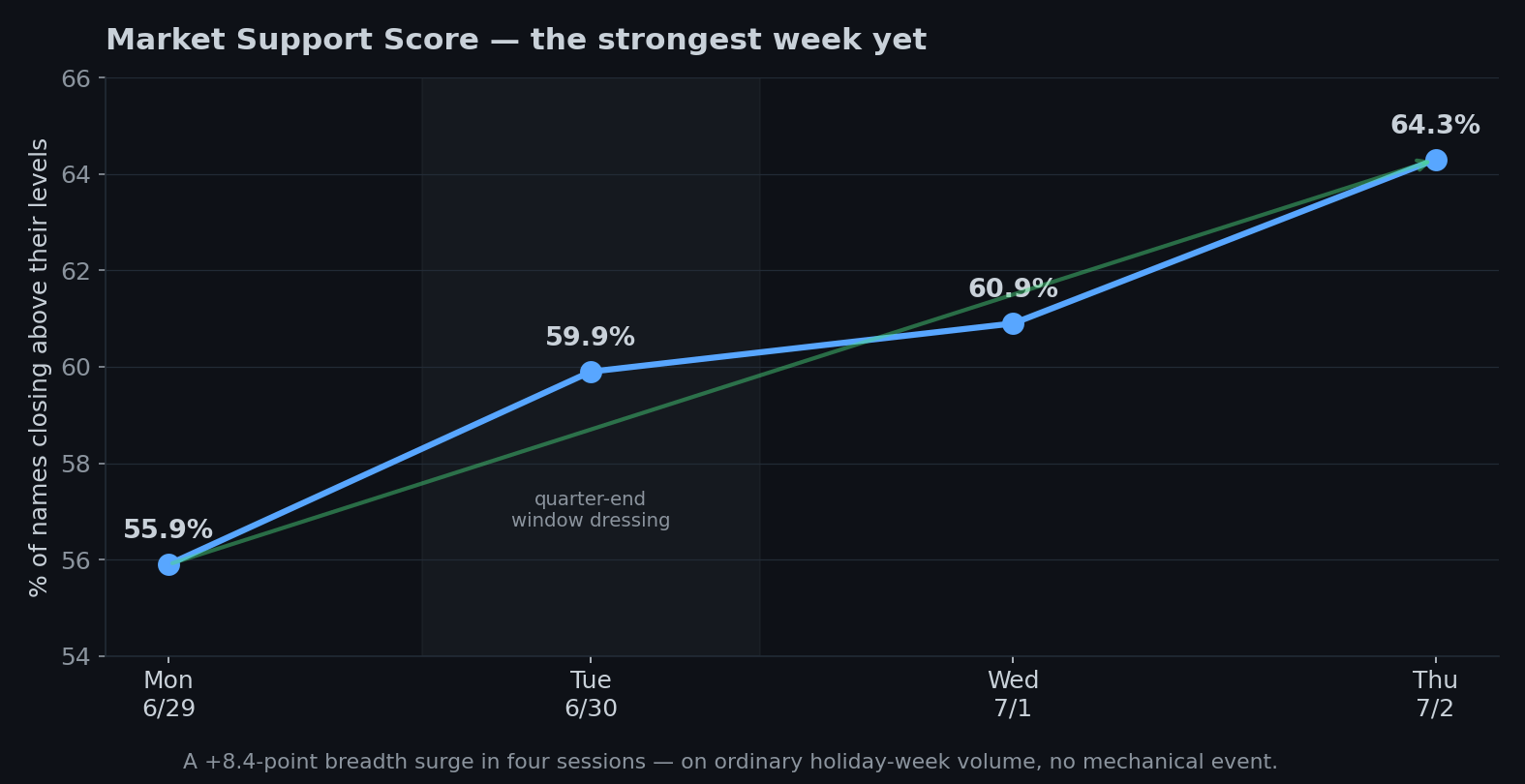

The share of stocks trading above the prices where institutions are positioned climbed four sessions straight — 55.9% Monday to 64.3% Thursday. That’s the strongest breadth reading in several weeks, an 8.4-point jump in a four-day, holiday-shortened week that most of Wall Street spent mentally at the lake.

And it happened on ordinary volume. Last week I told you the market’s record-breaking Friday was mostly the Russell reconstitution — a mechanical event, funds forced to trade by the rulebook, not conviction. This week there was no such asterisk. No index rebalance, no quad-witching, no forced anything. Just steady, unglamorous, real buying, accelerating into a long weekend. When breadth improves on a mechanical day, shrug. When it improves like this — quietly, on a Tuesday nobody cared about, especially with a large positioning event in the rearview mirror — pay attention.

Now, in terms of aggregate notional money sloshing around, the technology bucket is, and will for the foreseeable future continue to be, #1. Tuesday was June 30, quarter-end, and some of that day’s pop is “window dressing” — fund managers tidying up their holdings so the quarter-end statement looks respectable. But window dressing is a one-day cosmetic. More importantly, the climb kept going Wednesday and Thursday on genuine holiday-thin volume, and that part is real. And if we can agree that positions are the expression of informed institutional risk-taking, then all we need to monitor is post-print price action to determine whether institutions are endorsing or abandoning those theses.

Now the twist: look who was leading

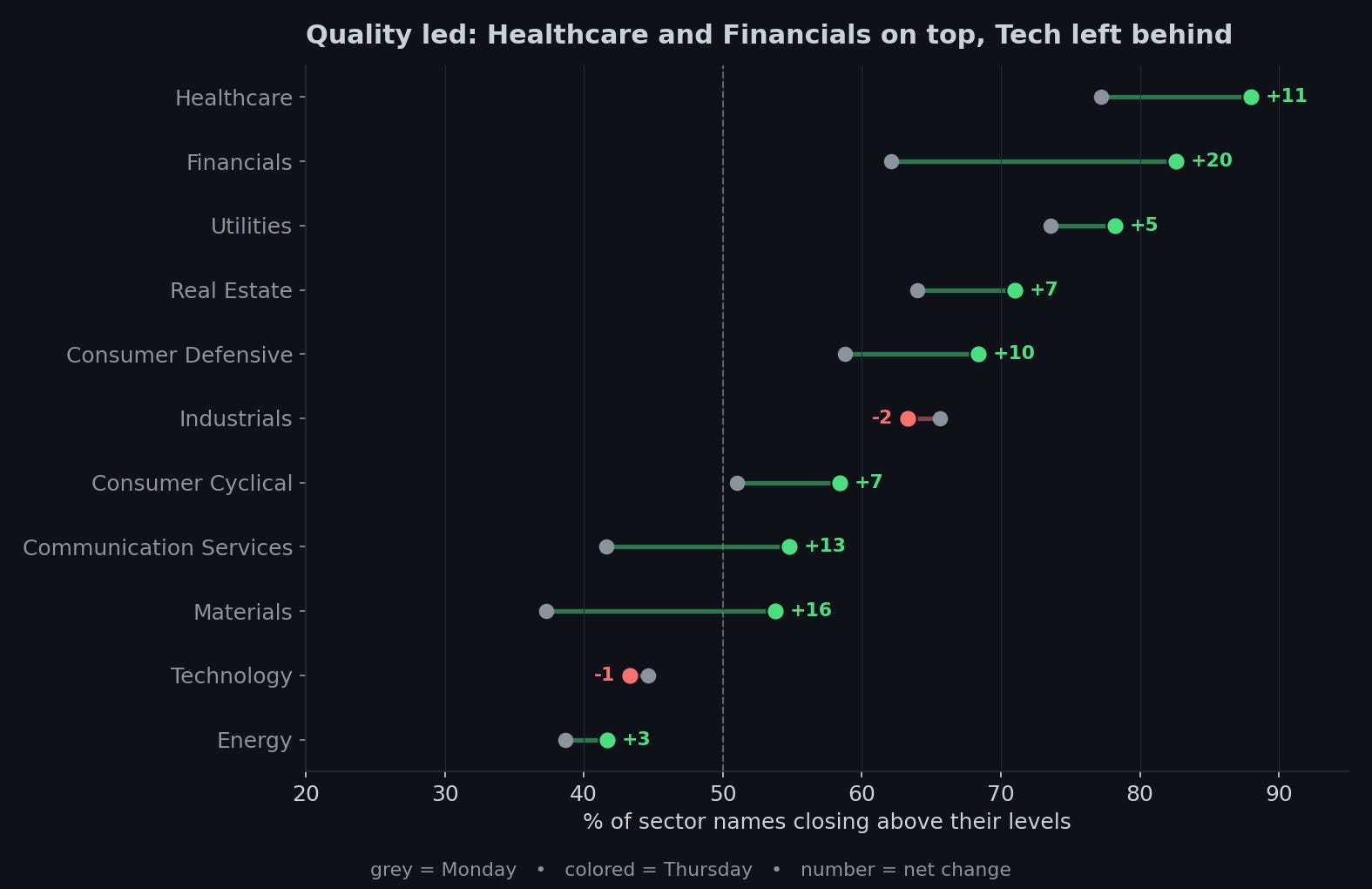

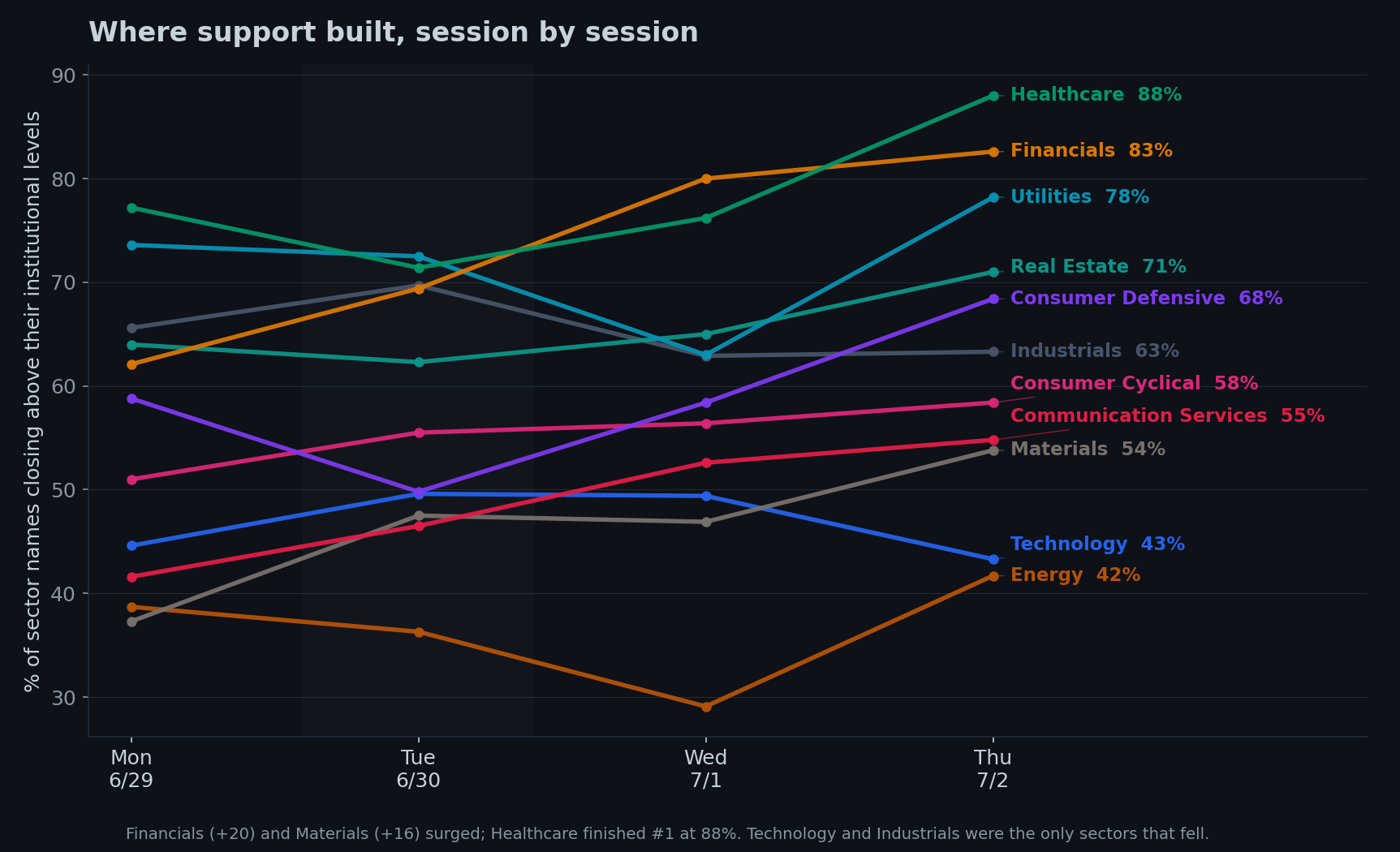

If I told you the market just had a big broad rally and asked you to guess the leader, you’d say technology. You’d be wrong. Technology fell this week, finishing near the bottom of the board at 43%.

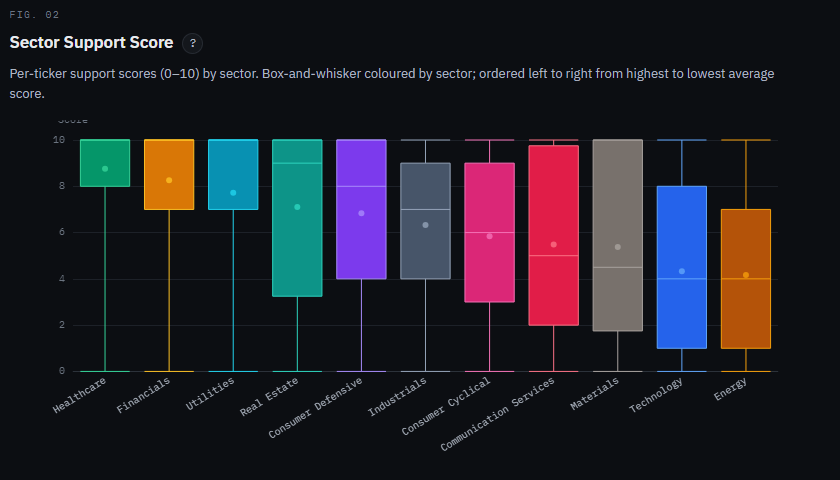

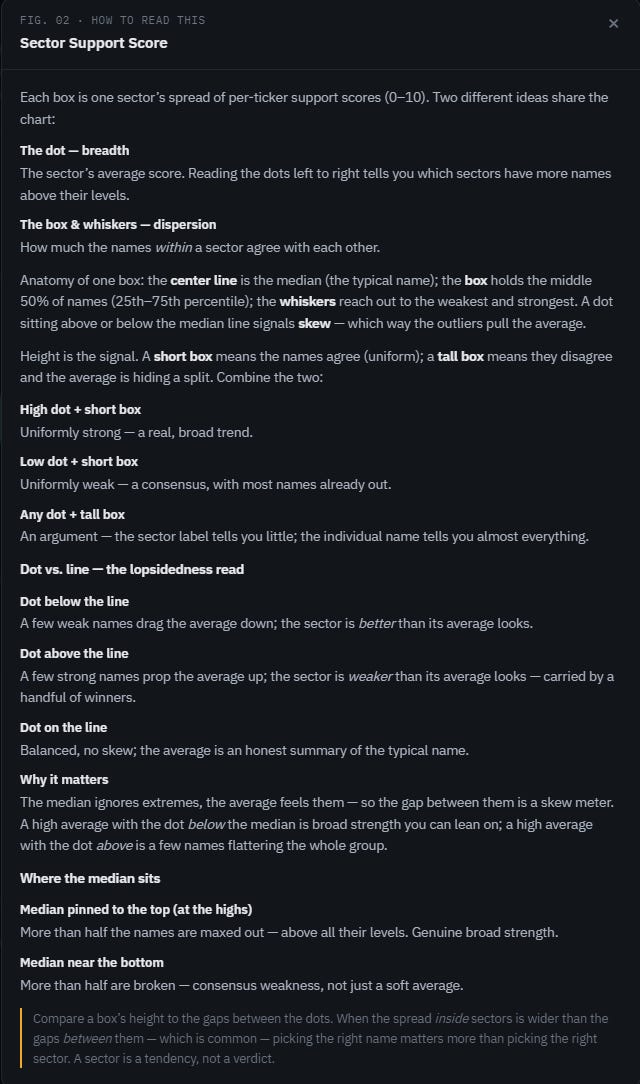

Quick refresher on how to read this whisker plot because it communicates a lot:

The sector that closed on top? Healthcare, at 88% — nearly nine of every ten names above a resounding majority of their institutional levels. Right behind it, Financials surged 20 points to 83%, the single biggest move on the board. Materials jumped 16. Communication Services jumped 13. The rally was led by the boring, the cheap, and the un-loved — quality and value — while the crowded megacap-tech trade that has carried this market all year sat the week out.

As a matter of fact, the tech weakness was global: there was clear profit-taking in high-priced tech and semis in Japan, and rotation away from highflying technology in China. The whole world spent the week selling the same crowded things and buying the same neglected things.

The Healthcare tell the headlines missed

Here’s where I think I can show you something the consensus is underplaying.

Everyone’s writing about Financials and the tech sell-off. Almost nobody is leading with Healthcare — and Healthcare is the strongest sector I have, at 88%. So I went looking for corroboration, because a single dataset saying something surprising is a hypothesis, not a fact. I found it in four different places.

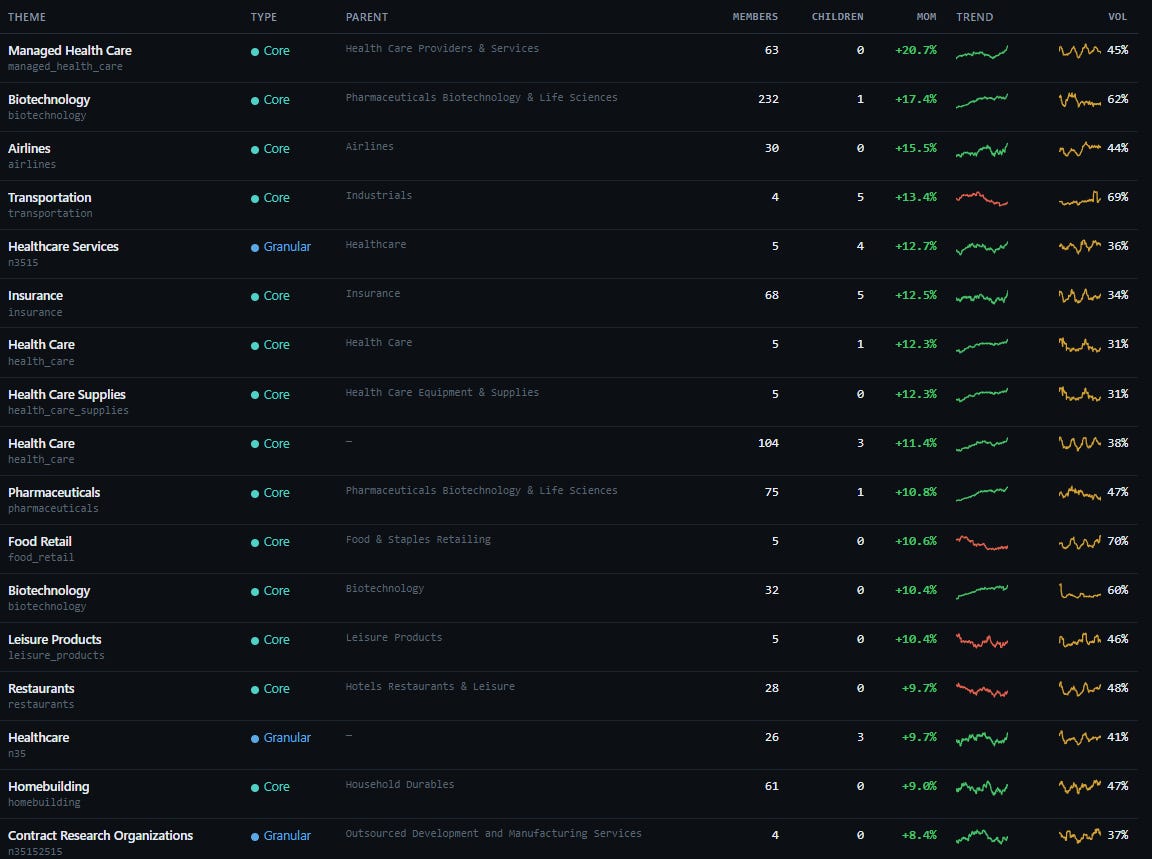

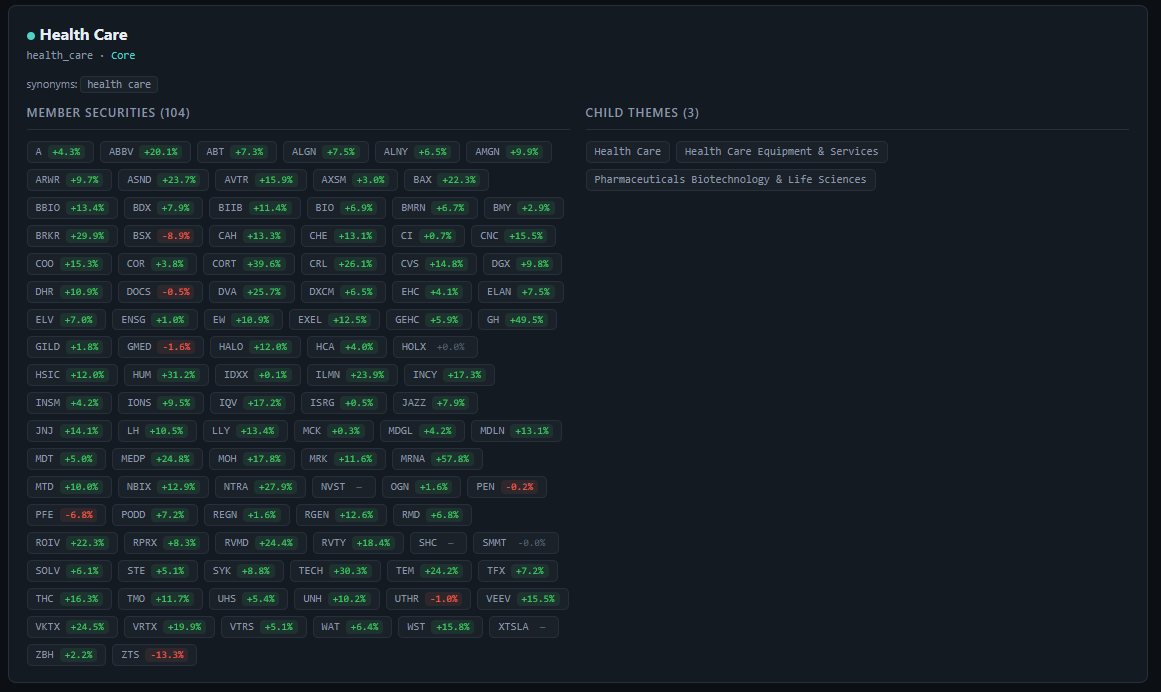

My support data has Healthcare first as seen in the sector whisker plot above. My own sector-rotation screen — which uses a completely different, more granular taxonomy — puts Health Care, Biotechnology, Insurance, and Managed Care all in the “leading” quadrant, strong and still improving, with the kind of broad membership (100-plus names) that means it isn’t three big stocks faking a trend; just look at these names all lit green (measuring momentum), you’d have to try deliberately to miss:

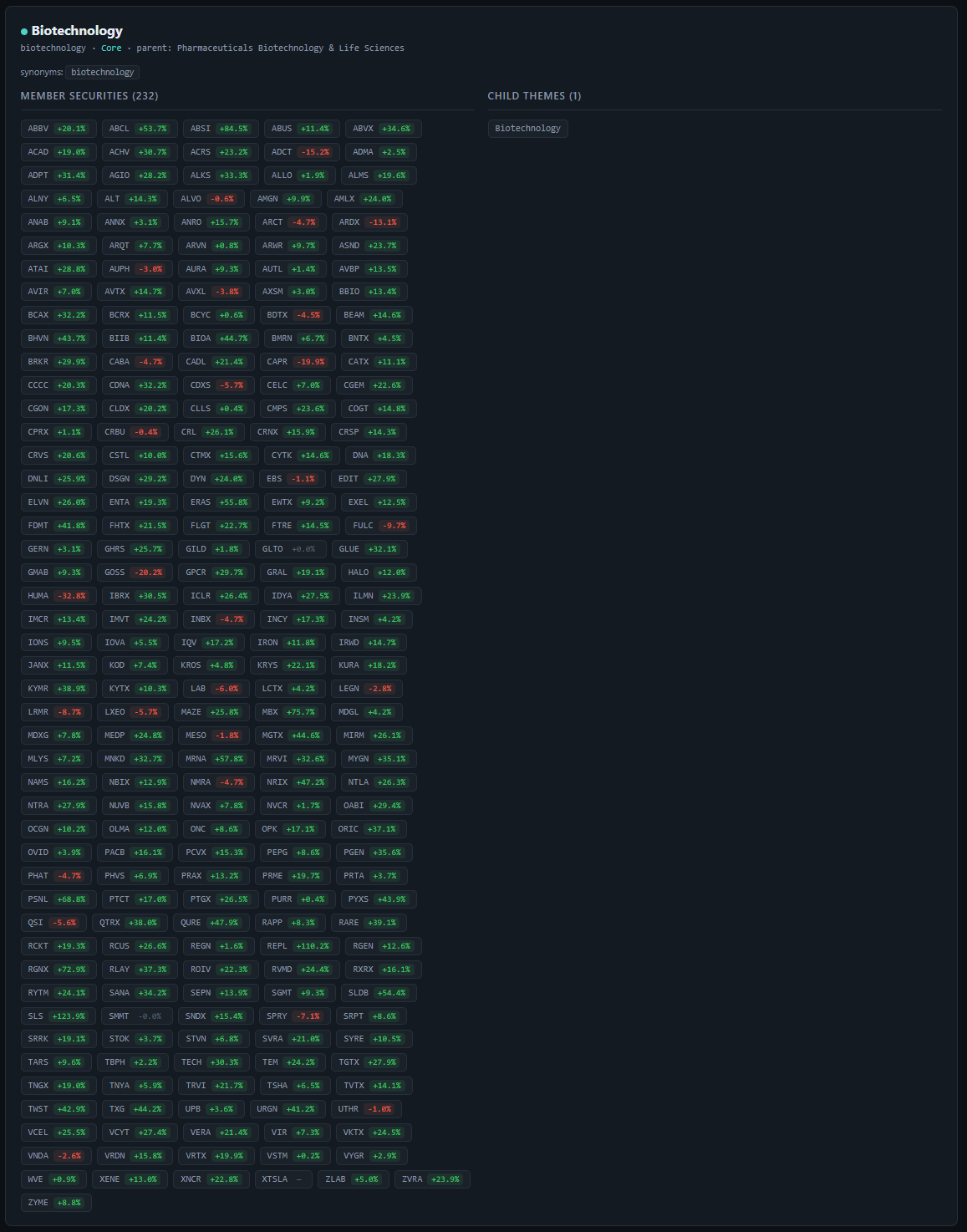

Biotech is also quietly resolving its consolidation pattern. This group is even larger and as stunningly and uniformly green:

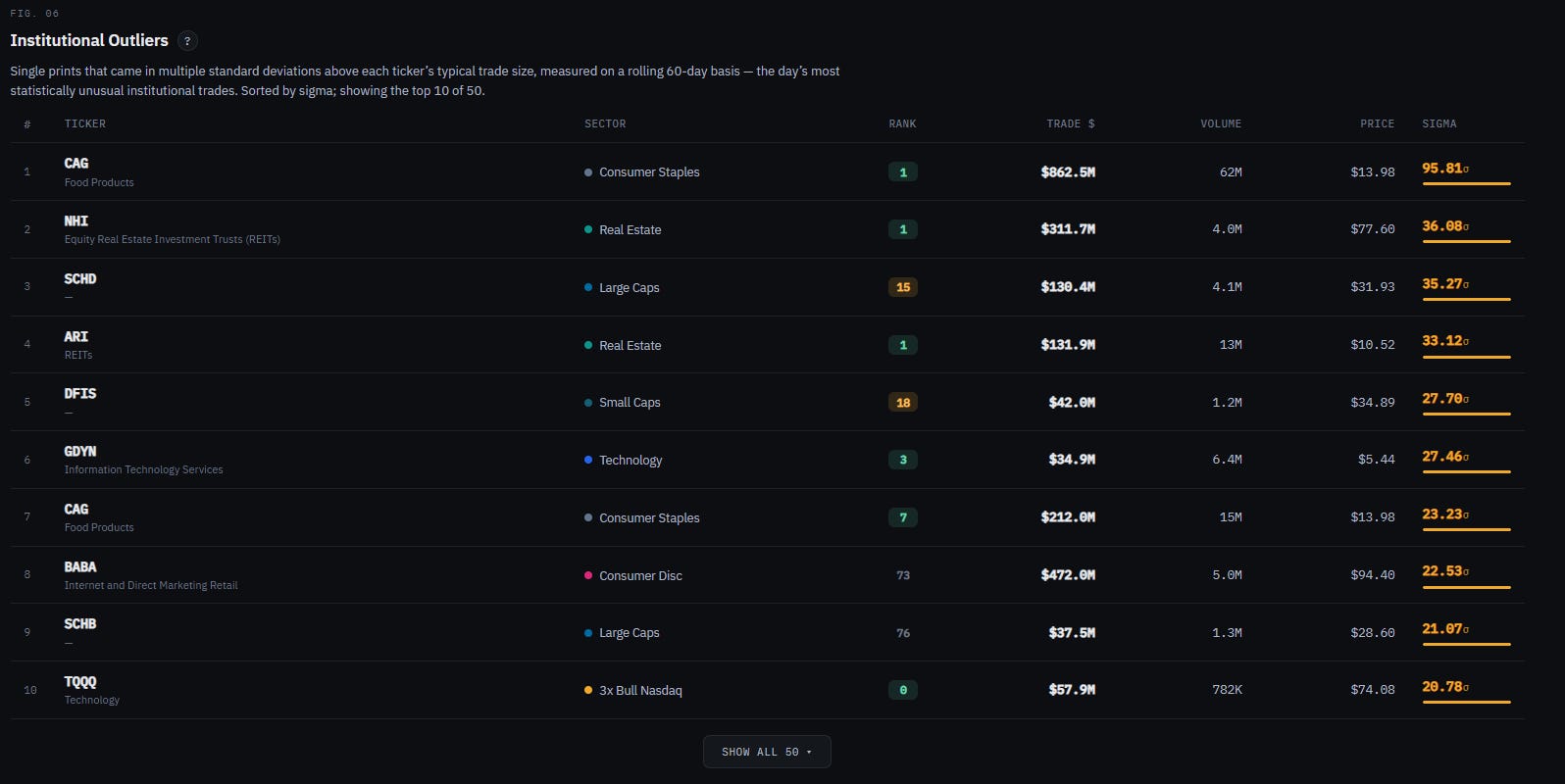

And the flow underneath all of this fits: the single most statistically extreme print of the entire week was Conagra — a packaged-food company, about as far from a sexy momentum stock as exists — trading nearly 96 standard deviations above its normal size.

When the weirdest trade of the week is a quiet defensive name and the strongest sector is Healthcare and your other screen agrees and you’ve got historically seasonal tailwinds at your back, that’s probably not coincidence - that’s a signal wearing a very boring disguise.

Four instruments, four different methods, one answer. That’s the kind of thing worth telling you about before it’s obvious to everyone.

Two more threads, both pointing the same way

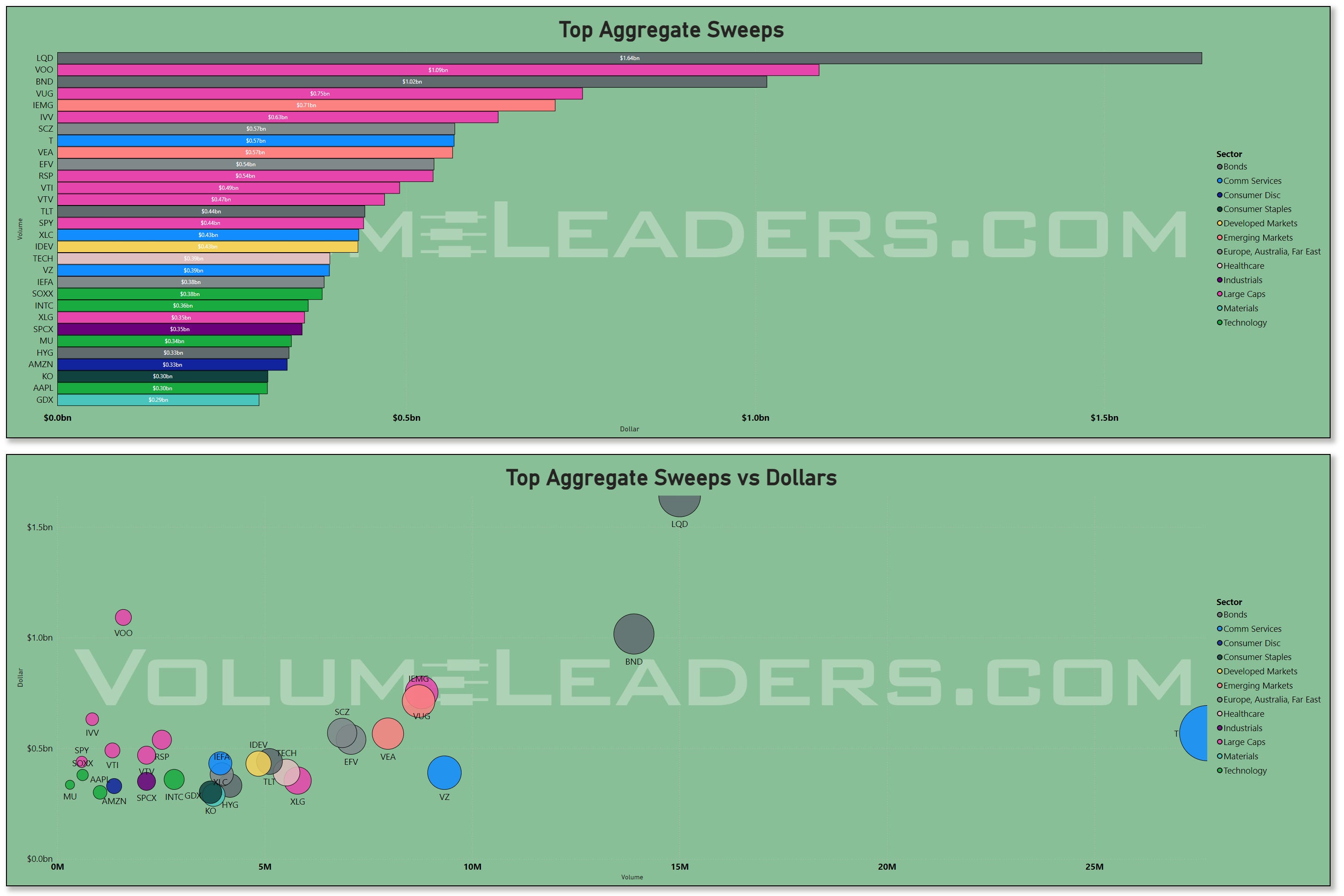

Abroad. The aggressive sweep money this week went international in a way I haven’t seen it do before — emerging markets, developed Europe, the whole alphabet of foreign ETFs, hoovered up in size. If you’re a regular reader, you know this is a thematic I’ve been tracking for a couple of years. This trade might be getting long in the tooth but the outlier prints show foreign developed-market funds appearing over and over at extreme sizes. And the fundamentals cooperate — European stocks had a strong week, eurozone inflation cooled to 2.8%, Germany’s market jumped nearly 4%. Many funds have taken an overweight emerging markets view, explicitly as an alternative to US technology and many news/research outlets are still constantly pushing opportunities outside of the US. If you’ve spent a decade assuming the only game is US megacap tech, there are enough independent voices and all of the evidence I’ve provided from the tape telling you the map is bigger.

Credit. The number-one sweep target of the entire week wasn’t a stock. It was LQD — investment-grade corporate bonds — swept at over $1.6 billion, with the broad bond aggregate right behind it. Aggressive money reaching for credit is a risk-on signal, not a hide-under-the-bed one; it means institutions are comfortable enough to lend to companies and get paid for it. Take a look around and credit conditions are still providing the green light for stocks. The bond market, in its unshowy way, was flashing the same all-clear as the stock market.

So is this the good kind of rally or the nervous kind?

A market led by Healthcare and consumer staples sounds defensive — money hiding in things people need regardless of the economy. But a market led by Financials and Materials sounds like the opposite — those are pro-cyclical, they want growth and a steeper yield curve. This week did both at once, which is unusual, and it can mean one of two things.

The bullish read: this is a healthy broadening. The rally stopped depending on seven megacap names and spread out to the entire market — quality, value, cyclicals, defensives, everything except the crowded tech trade that needed a rest. Broad rallies are sturdier than narrow ones. This is what the early innings of a durable leg look like.

The cautious read: this is a quiet flight to quality. The market is going up, but the character of what’s leading — healthcare, staples, dividends, investment-grade credit — is what you’d buy if you wanted to stay invested but sleep at night. Money that’s climbing the wall but keeping one hand on the exit.

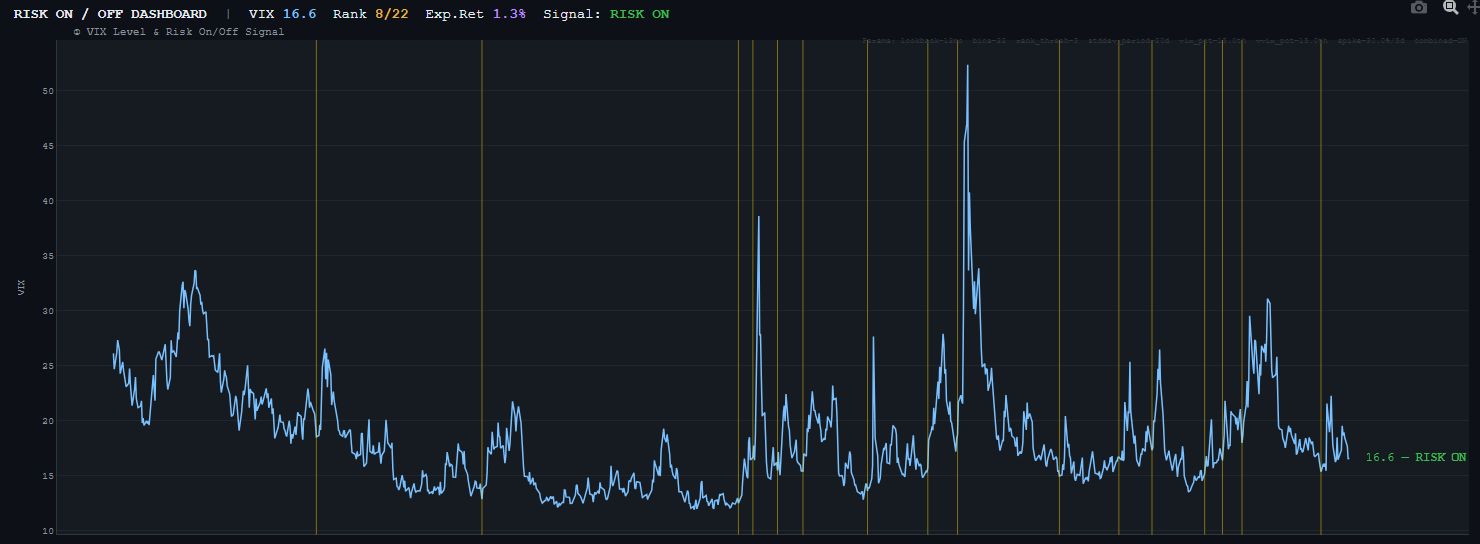

Here’s what I’m really looking for in coming sessions: if Technology starts clawing back above institutional participation levels while Healthcare and Financials hold — everybody rising together — it’s a real broadening, and you lean in. If tech keeps bleeding and only the defensive-and-quality complex holds the line, it’s a rotation into the bunker, and you respect it. Right now it’s genuinely poised between the two. The next two weeks of tech will tell you which movie you’re watching. Vol is cooperating right now, too and systems are saying risk-on:

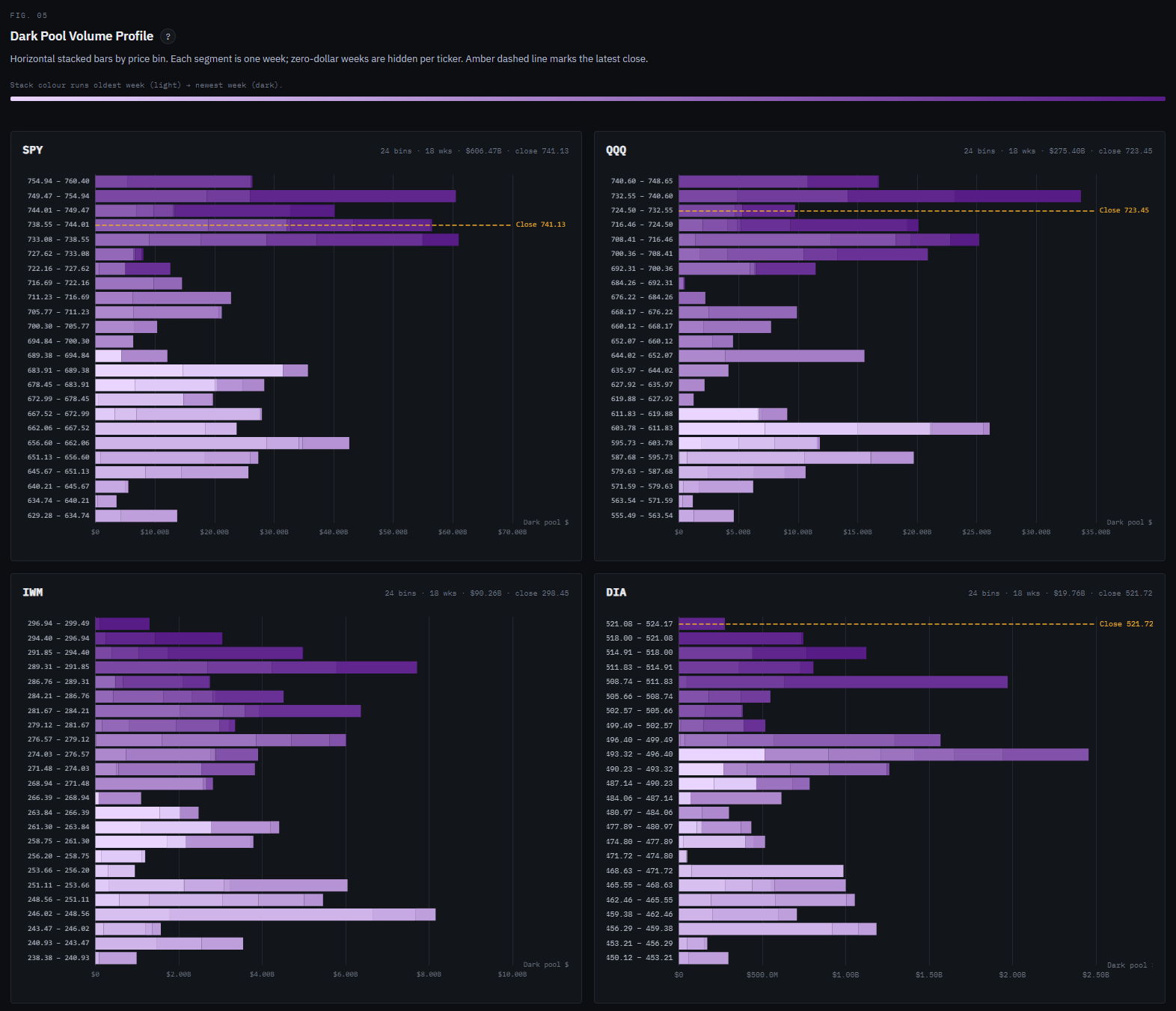

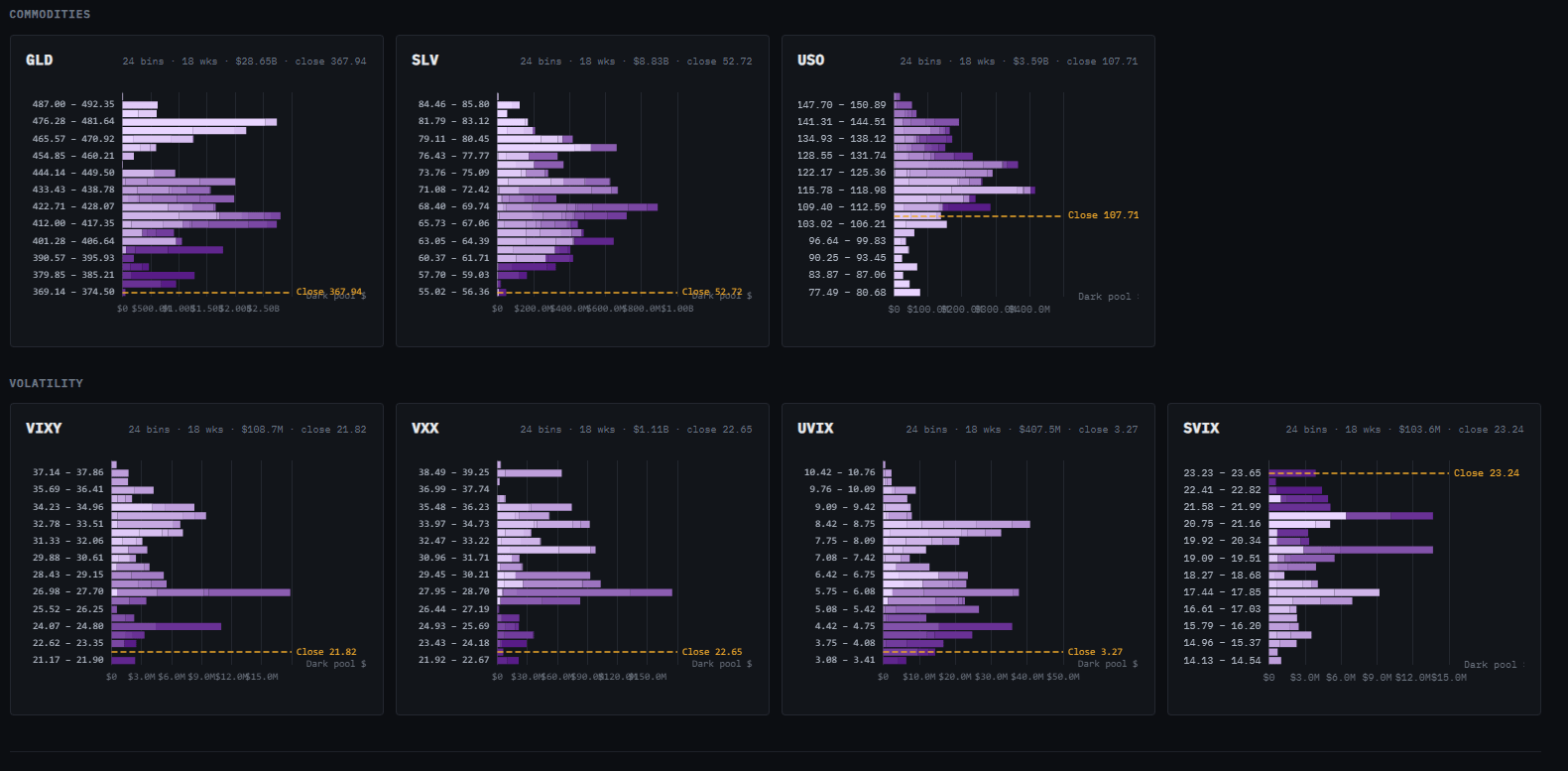

Here’s a glance at institutional positioning in the majors and some common ETFs for you to chew-on this holiday weekend and a quick primer for those new to the format. Note the overhead shelf in XLK as it pertains to what I just mentioned that I’m looking for in tech.

What this means, by your clock

If you trade in days to weeks: the broadening is the trade, and the tape, the sweeps, and the seasonal calendar all lean the same way — lighten hedges and add risk for the summer-rally window. It’s early-July-thin, the leadership is quality over momentum, and a soft jobs number means the economy is “fine,” not “hot.” Trade the rotation — quality, financials, international — not the megacap-tech reflex. And keep an eye on that tech-support tell.

If you invest in months to years: the useful signal this week is participation. A market where 64% of names are above their levels, led by real earnings sectors instead of a handful of stories, is a healthier market than the narrow one we’ve had. The backdrop — a steadying “Goldilocks” jobs market, oil back under $70, a Fed likely on hold — is a decent floor under things right now. None of that tells you what next month does. It does suggest a portfolio built only around the famous seven names is narrower than the market has quietly become — again.

The through-line, same as always: the headlines will tell you what was loud. The quiet weeks tell you what’s true. This week the money spent a sleepy holiday half-session buying health care, banks, foreign stocks, and corporate credit, and left the crowded trade alone. That’s worth more than a hundred loud Fridays.

Enjoy what’s left of the long weekend. Wishing you a calm holiday, a full plate, and the good sense to trust the quiet data over the loud noise.

Thank you for being part of this community and for investing your time in this week’s edition. The quality of this readership — thoughtful, disciplined, engaged — is what makes this work meaningful. I’m grateful to build alongside you. Here’s to a week of clarity, conviction, and well-executed opportunities.

— VolumeLeaders